Home Loan Prepayment: If you have got the lump sum amount from any other source then you can get your EMI reduced by prepayment.

Home Loan Prepayment: Prepayment is a better option to get rid of the loan and its interest. We all want to pay off our debts as soon as possible and get rid of long term financial commitments. If you have got the lump sum amount from any other source then you can get the EMI reduced by prepaying. The principal amount i.e. the amount taken in the loan is adjusted from the pre-paid amount and if this amount is reduced then its effect will be seen on the EMI.

RBI recently increased the repo rate by 40 basis points, after which many banks have increased the lending rate. Due to this, taking a loan has become expensive now. Most of the floating interest rate loans are linked to the repo rate. Due to which the EMI of the borrowers is increasing. Let us know how you should manage prepayment of home loan and what are its benefits in the long term.

Income Tax: Salary arrears has increased the tax burden? You can get relief under section 89, understand the calculation

How does the increase in interest affect loan repayment?

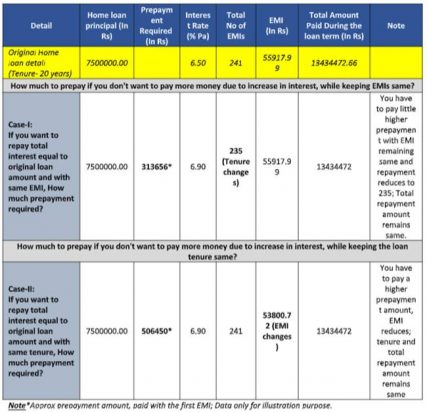

When the interest rate on your existing loan increases, you get two options from the lender – either your EMIs increase (option I in the example below) or your tenure increases. (Option II in the example below). With the help of the examples in the table below, let us know what happens to your loan in both the cases.

In both the cases, borrowers will have to pay higher interest, however, if you do not change the EMI and extend the tenure, then you will have to pay higher interest. Loan prepayment can be a better way to reduce the impact of interest rate hike on your loan.

India Weather Update: Relief from heatwave in North India for 1 week, heavy rain expected in Kerala-Karnataka, IMD estimates

How is the loan prepayment done?

According to BankBazaar, when the interest rate rises, and you want to prepay during the loan term to avoid additional interest, the bank gives you various options to re-adjust your loan liability. The first option is that (Case-I in the example below), there is no change in EMI, while the repayment tenure changes. As a result, the number of EMIs comes down. Another option is that (in example Case-II), the size of the EMI changes while the tenure remains the same. But it requires a higher pre-payment and you get the benefit of reduction in EMI size.

You should be prepared with the right repayment strategy. There may be several repayment options available with your lender which can help you save interest and avoid any kind of stress. So, don’t hesitate to discuss with your lender and choose the right option for you.

(Sanjeev Sinha)

www.financialexpress.com